Roth Conversion

What is Roth Conversion?

A Roth Conversion allows you to move money from a traditional IRA or 401(k) into a Roth IRA. You pay taxes on the amount converted today, but future qualified growth and withdrawals will become tax-free.

For many retirees, the goal is not simply to grow wealth, it’s to create more control over future taxes and retirement income.

Roth Conversion Can Help:

📈 Reduce Future Taxes

Traditional retirement accounts are taxable when withdrawn. A Roth Conversion may help reduce how much of your future retirement income is exposed to taxes later.

💣 Lower Future RMD Pressure

Traditional IRAs are subject to Required Minimum Distributions (RMDs). Converting portions to a Roth IRA may reduce future mandatory taxable withdrawals.

🩺 Help Manage Medicare Premium Increases

Higher retirement income can increase Medicare Part B and Part D premiums (IRMAA). Roth income is generally not included in those income calculations.

🏛️ Reduce Social Security Tax Exposure

Large taxable withdrawals can cause more of your Social Security benefits to become taxable. Roth withdrawals can help create more flexibility in managing taxable income.

⚙️ Create More Flexible Retirement Income

Having both taxable and tax-free income sources may give you more control over when and how you withdraw money in retirement.

👨👩👧 Help Protect Your Legacy

Traditional IRA balances passed to heirs can create future tax burdens for beneficiaries. Roth assets can provide more tax-efficient inheritance opportunities.

🔒 Create More Predictable Taxes

Many retirees worry about future tax rates increasing. Some choose Roth conversions to pay taxes strategically now rather than face uncertainty later.

A new way to optimize your accounts.

The only retirement account the IRS can't tax.

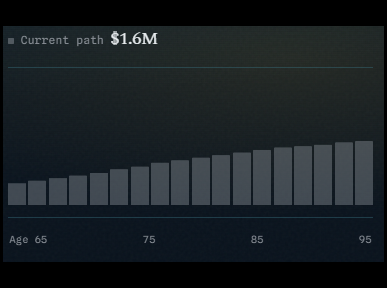

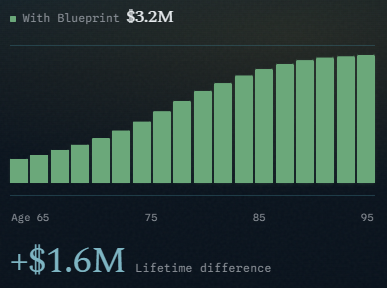

✔️ Up to 97% more Lifetime Wealth

Example: 65 with a $500K IRA, married, filing jointly.

Designed to do 3 things.

💵 No Out-of-Pocket Costs

Most retirees keep only 4–7% of their savings in cash, which doesn't leave much room for large tax hits. A Roth Blueprint covers the taxes using the strategy itself, not your savings. We'll help you convert without emptying the coffers.

🚫No Jumping Tax Brackets

Converting too much can push you into a higher marginal bracket. A Blueprint will help you convert right up to the top of your current tax or IRMAA bracket each year, never a dollar over. You convert as much as you can without bumping into a higher rate.

🛡️No reduction of income.

Any Roth conversion will alter your tax landscape, but the benefits won't be worth it if the conversion shrinks your bottom line. We model your conversions so that your lifestyle needs are always prioritized before, during, and after the conversion.

What do I get when I run my numbers?

Roth Blueprint tests every tax bracket and every IRMAA tier against your account size; filing status, and current income.

Your Blueprint report, based on hundreds of iterations, clarifies the lifetime potential of a Roth conversion.

- Scenarios tested 400+

- Optimal path Identified

Nine questions, up to 97% more lifetime wealth.

Free . 2-3 minutes . Secure